What Happens When You Ignore IRS Notices

- Marion Davis

- May 29

- 6 min read

From notices to liens, levies, collections, and lost resolution options

IRS notices have a special talent for showing up at the worst possible time.

You open the mailbox, see the government seal, and immediately decide today is not the day. So the notice gets placed in the official taxpayer filing system: a kitchen counter pile, a desk drawer, the passenger seat of your car, or somewhere “safe” where it will never be seen again.

Understandable? Yes. Smart? Absolutely not.

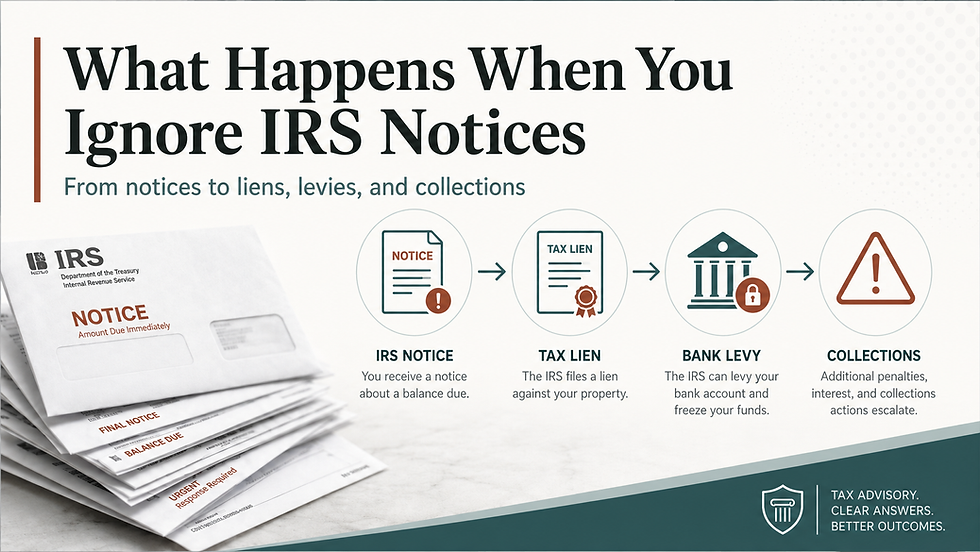

Ignoring IRS notices does not make the problem go away. It usually makes the problem more expensive, more stressful, and harder to resolve. The IRS collection process is not instant, but it is progressive. It starts with notices and balance-due letters. If ignored long enough, it can move into tax liens, levies, enforced collections, and fewer resolution options.

The IRS does not need you to agree, respond, or participate for the process to continue. Silence is not a strategy. It is usually interpreted as nonpayment.

The First IRS Notice Is Usually Not the Disaster

Most IRS problems start with a notice. It may say you owe a balance, there was a mismatch between your tax return and third-party reporting, a payment was not applied correctly, or additional information is needed.

At this stage, the issue may still be very manageable.

Sometimes the IRS is right. Sometimes the IRS is wrong. Sometimes the taxpayer is right, but the documentation was incomplete. Sometimes a payment was made but posted to the wrong year, because apparently tax payments enjoy taking scenic routes.

The important point is this: the first notice is often your best opportunity to correct the issue before it turns into a collection matter.

The IRS collection process generally begins after the IRS assesses the tax, sends a bill explaining the amount due, and the taxpayer does not fully pay on time. That means the notice is not just informational. It is the beginning of a timeline.

Penalties and Interest Keep Moving

One of the biggest mistakes taxpayers make is assuming the balance on the notice is frozen.

It is not.

Penalties and interest generally continue to accrue until the balance is paid or otherwise resolved. So a tax bill that feels annoying today can become a much larger problem months later. This is especially frustrating when the original issue could have been addressed early with a payment plan, correction, penalty relief request, amended return, or documented response.

Ignoring the notice does not pause the math. The IRS is very committed to math.

For business owners, this can become even more serious. Payroll tax issues, unpaid employment taxes, and business tax debts can create additional exposure, including potential trust fund recovery penalty issues in certain cases. Once a business tax problem moves into collections, the IRS may ask for financial information, business records, bank details, and proof of current compliance.

In plain English: the longer the issue sits, the less casual the conversation becomes.

Notices Can Progress Toward Liens

A federal tax lien is the government’s legal claim against your property when you neglect or refuse to pay a tax debt after the IRS assesses the liability and sends a Notice and Demand for Payment. The IRS may then file a public Notice of Federal Tax Lien to alert creditors that the government has a legal right to your property.

This matters because a lien can affect more than your relationship with the IRS.

It can interfere with financing, refinancing, selling property, business credit, and general financial flexibility. For business owners, that can be a major problem. You may be trying to secure a line of credit, purchase equipment, sell a building, or clean up your balance sheet. A tax lien can become an ugly obstacle sitting right in the middle of that process.

A lien does not necessarily mean the IRS is taking your property immediately. That is a common misunderstanding. But it does mean the government is protecting its interest in what you own.

That is not a small step.

Then Come Levies

A levy is more aggressive than a lien.

A lien is a claim. A levy is a seizure.

The IRS describes a levy as the legal seizure of property to satisfy a tax debt. It can include wages, bank accounts, vehicles, real estate, personal property, and other rights to property.

This is where taxpayers often stop ignoring the problem, usually because the problem has stopped being theoretical.

A bank levy can freeze and remove funds from an account. A wage levy can affect ongoing income. A levy on business accounts can disrupt payroll, vendor payments, rent, and operations. For a business owner, this can go from tax issue to a cash flow emergency very quickly.

The IRS does have procedures before certain levy actions. For example, a formal Final Notice of Intent to Levy and Notice of Your Right to a Hearing generally gives the taxpayer an opportunity to request a Collection Due Process hearing before levy action proceeds.

But here is the part people miss: rights have deadlines.

If you ignore the notice, you may lose the best opportunity to challenge the action before it happens.

You May Lose Resolution Options

This is one of the most important reasons not to ignore IRS notices.

Tax resolution is not just about calling the IRS and asking nicely. There are structured options, and the best option depends on the facts. Possible resolutions may include installment agreements, penalty abatement, currently not collectible status, offers in compromise, and appeals options.

But waiting too long can narrow your options. If enforcement has already started, the IRS may require more documentation, faster action, and proof that you are current with filing and payment obligations. If deadlines for appeal rights pass, you may still have options, but they may be weaker or less protective.

In other words, the resolution conversation is much better when you start it before the IRS starts taking things.

Ignoring Notices Can Also Damage Your Position

When you respond early, you control more of the narrative.

You can explain the issue, provide documentation, request correction, propose a payment arrangement, or challenge the balance. When you ignore the IRS for months, the situation looks different. Even if you had a valid explanation, the lack of response can make the matter harder to unwind.

That does not mean all hope is lost. Many IRS problems can still be resolved after notices have been ignored. But the taxpayer may have fewer procedural protections, more accrued penalties and interest, and a much shorter runway.

This is especially true for taxpayers who have unfiled returns. The IRS may prepare a substitute return in some cases, and those returns often do not include all deductions, credits, basis information, or business expenses the taxpayer may have been entitled to claim. The IRS is not in the business of preparing your most tax-efficient return. Shocking, I know.

What You Should Do Instead

If you receive an IRS notice, do not panic. But do not ignore it.

Read the notice carefully. Identify the tax year, form number, amount due, response deadline, and reason for the notice. Compare it to your filed return, payment records, IRS account transcript, and supporting documentation.

Then determine the correct response.

Sometimes the answer is simple: pay the balance, set up an installment agreement, or send missing documentation.

Sometimes the answer requires more analysis: disputing the amount, correcting a return, requesting penalty relief, addressing payroll tax exposure, or evaluating formal resolution options.

The worst response is no response.

IRS notices are not love letters. They are not suggestions. They are part of a system that continues moving whether you participate or not. The earlier you address the issue, the more options you usually have and the less expensive the problem may become.

Ignoring IRS notices might feel easier in the moment. But eventually, the IRS tends to get your attention. And when that happens, it is almost never at a convenient time.

Do Not Wait Until the IRS Makes the Next MoveIf you have received an IRS notice, the best time to address it is before it turns into a lien, levy, or full collection problem. The earlier you respond, the more options you may have and the better chance you have of controlling the outcome. At Guidepost Tax & Advisory, we help taxpayers understand what the notice means, evaluate their resolution options, communicate with the IRS, and build a path forward that is compliant, practical, and legally sound. Ignoring the IRS rarely works. Having a plan does. Received an IRS notice or worried about a tax balance? |